The Indian food service market became a hot topic of discussion across social media recently, when Nikhil Kamath , Co-Founder, Zerodha, contrasted the eating out culture between India and Singapore. Observing that Singaporeans mostly don’t cook at home anymore and hardly have kitchens, he speculated how this trend, if replicated, may open up huge opportunity in the Indian food service market.

As the debate that raged over this suggestion indicates, Indian consumers at large are still not ready to ditch the kitchen! But the food services sector is undoubtedly in high growth mode. A report by Swiggy and Bain & Company last year estimated the Indian food services market at Rs 4-5 lakh crore in 2023, with an estimated CAGR of around 10-12% to reach Rs 9-10 lakh crore by 2030.

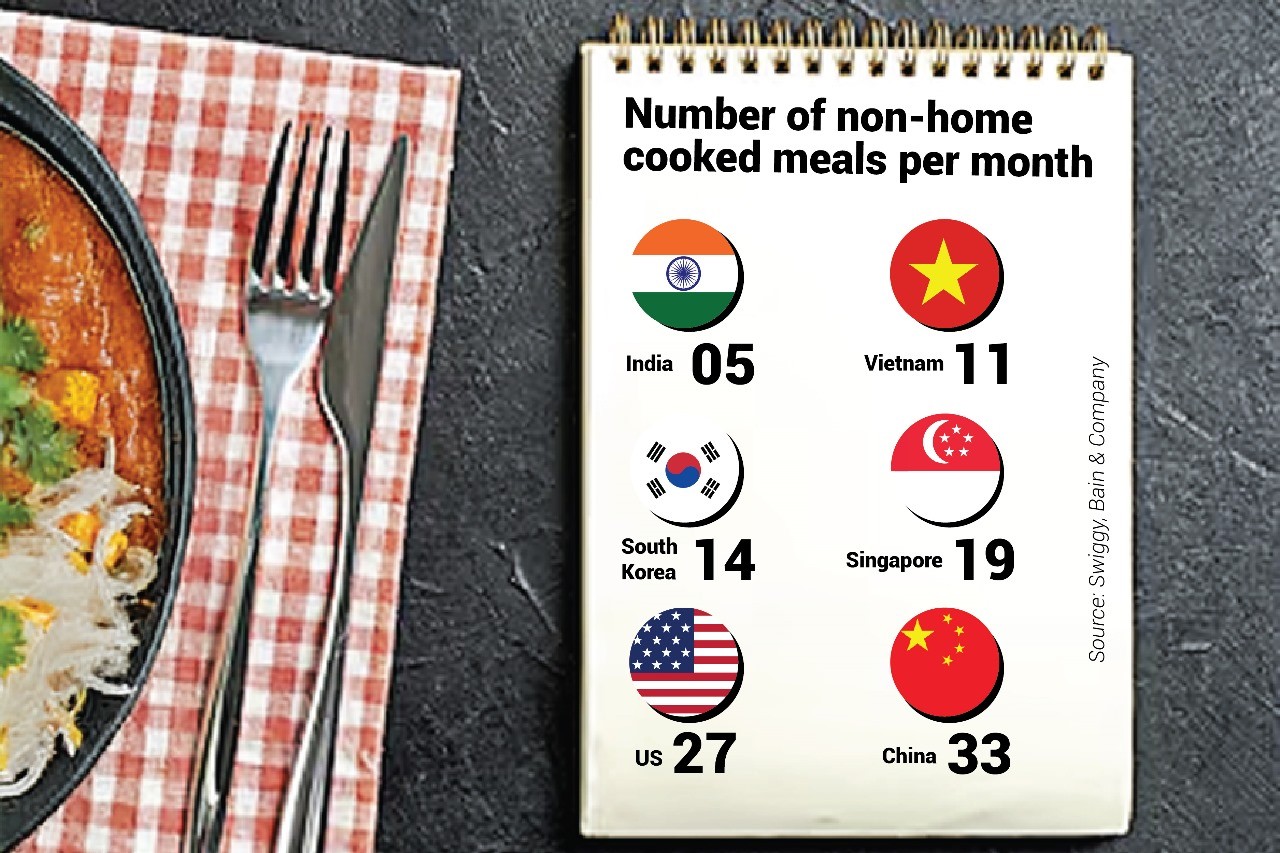

When you compare ‘eating out frequency per month’ to advanced markets like China (33), US (27), Singapore (19), South Korea (14) and Vietnam (11), India’s market (5) is still dominated by home cooked meals.

The report estimated that eating out in India is currently averaged at around 5 occasions a month, which could improve to around 7-8 times by 2030. From a special event, it is now become more of a convenient lifestyle, which marks a key shift in India’s consumer landscape. There is also discernable shift towards greater culinary variety with a number of international cuisines gaining acceptance, like Thai, Chinese, Italian, Lebanese, Mexican and pan-Asian.

However, when you compare this to advanced markets like China (33), US (27), Singapore (19), South Korea (14) and Vietnam (11), India’s market is still dominated by home cooked meals.

At the same time, there are strong drivers for the growth of this market in the coming years. India’s GDP per capita is projected to grow to US$ 4,000 by 2030, up by 70% compared to 2023, effectively making it a middle income country (Standard Chartered Bank).

Currently, according to the report by Swiggy and Bain & Co, around 70% of the food service demand is accounted for by the top 50 cities, and around upper middle income and high-income segments. Over the years, incremental growth is expected from Tier 2 cities and beyond. Gen Z is around 40% of the consumer group that has a high propensity to eat out. As their purchasing power grows, the trend is expected to accelerate further.

Further, a report by Deloitte and Retailers Association of India projects that the number of people with per capita income >US$ 10,000 is expected to triple to reach 165 million by 2030. This is expected to bring a strong and fundamental shift towards discretionary spending, with the following fundamental drivers, according to the report:

Premiumisation and evolving consumer preferences: With increasing affluence, Indian consumers are placing greater emphasis on quality, convenience, and experiences rather than just price. Gen Z and millennials, making up 52% of the population, are at the forefront of this transformation, fueling demand for premium brands, sustainable products, and personalized offerings.

Digital and financial inclusion driving spending: Credit card penetration in India is projected to triple from 102 million in 2024 to 296 million by 2030, driving higher consumer spending. Fintech innovations and digital payment solutions like UPI are transforming consumer interactions with brands, accelerating e-commerce growth and fueling a new era of digital-first consumption.

Shift in household spending patterns: With rising disposable incomes, the share of food in total spending has declined—rural households saw a drop from 60% to 47%, while urban households fell from 48% to 40%. This shift highlights a growing preference for dining out, travel, wellness, and discretionary categories like fashion, fitness, home improvement, and consumer durables.

Rise of organised retail and experience-led consumption: Organised retail is growing at a robust 10% CAGR and is set to reach US$ 230 billion by 2030. Consumers are gravitating towards experience-driven retail, omnichannel shopping, and hyper-personalised services, compelling brands to innovate their engagement strategies.

India’s food services industry is attracting investments from a variety of players, including established firms as well as startups, who are bringing in disruptive business models. The market is evolving rapidly, driven by changing consumer preferences, technological advancements, disruptive influence of startups and shifts in the economic landscape.

Some of the traditional models that continue to enjoy customer favour are:

Fine Dining Restaurants

High-end, full-service restaurants offering premium cuisine and ambiance.

Examples: Indian Accent New Delhi’, Bukhara, OLIVE BAR AND KITCHEN PRIVATE LIMITED.

Casual Dining Restaurants (CDRs)

Mid-range restaurants providing quality food and service but with a relaxed ambiance.

Examples: Barbeque Nation Hospitality Ltd., Moti Mahal

Quick Service Restaurants (QSRs)

Fast food chains offering limited menus, standardized food, and quick turnaround.

Examples: McDonald’s, Domino’s, Haldiram’s.

Cafés and Bakeries

Outlets focused on coffee, tea, and light food options like sandwiches and pastries.

Examples: Starbucks, Cafe Coffee Day, Chaayos

Street Food Vendors & Dhabas

Unorganized yet popular, these offer regional and affordable food options.

Examples: Local chaat stalls, paratha dhabas on highways.

Institutional Catering

Companies providing large-scale food services to schools, colleges, corporate offices, and hospitals.

Examples: Sodexo, Compass Group.

Tech integration is key to the development of these models, which inculcate AI-powered recommendations, automation in food prep, and digital payments. Moreover, the rise of diet-specific and organic meal services promises to widen the market and bring more health conscious Indians to restaurants than before.

India’s food industry is embracing eco-friendly packaging and zero-waste kitchens as sustainability gains traction. Rising consumer awareness, government regulations on single-use plastics, and cost benefits are driving this shift. Restaurants are adopting biodegradable, compostable, and edible packaging while minimizing food waste through smart inventory management and surplus food donation programs.

The rise of diet-specific and organic meal services promises to widen the market and bring more health conscious Indians to restaurants more often than before.

Several resaurants are switching to paper-based and plant-based packaging. Cloud kitchens are optimizing portion sizes to reduce excess waste. With Gen Z and millennials prioritizing sustainability, businesses that adapt to greener practices are gaining a competitive edge while reducing their environmental footprint.

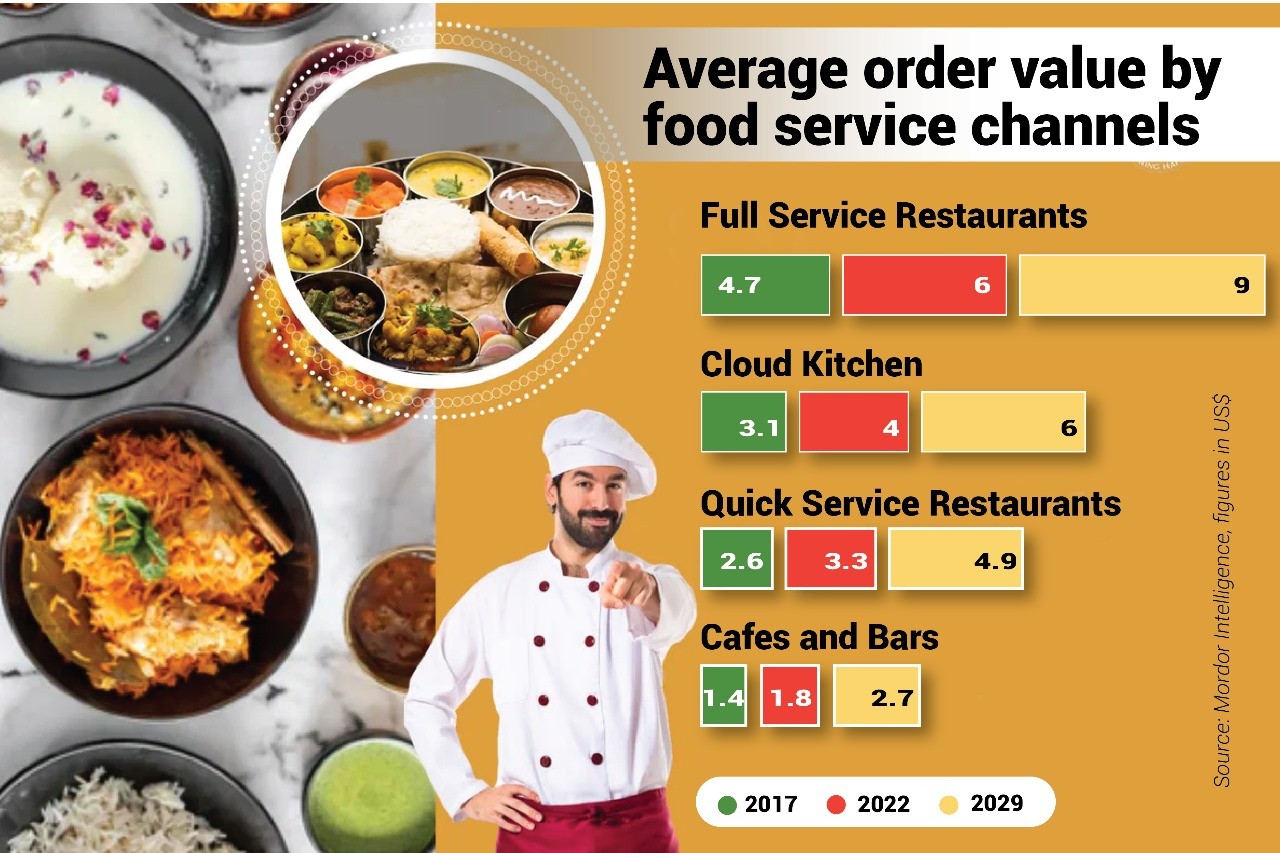

A report by RedSeer Consultants projects online food services market to grow at a CAGR of 17-22% to reach US$ 23-30 billion by 2030. The offline food services market is projected to grow at a CAGR of 13-17% to reach US$ 60-74 billion by 2030.

A range of innovations are driving growth in both segments. Recent examples include initiatives by Zomato and Swiggy to enhance their services with offerings like scheduled, large order fleet, cancelled orders at discounted prices, 10-15 mins deliveries etc. Similarly, marketers are encouraging more usage through launch of delivery-only brands, menus, cuisines, occasion-based menus, etc.

The instances of dining out are increasing. Around 50% of Metro and Tier-1 consumers are showing an increasing propensity to dine out/order in with monthly spends upwards of ₹ 2000 according to the RedSeer survey.

A very pertinent trend for both international and Indian brands is that consumers are increasingly seeking variety, be it for flavor waves (long term trending on Google Search) like Vietnamese Coffee and Tteokbokki (simmered Korean rice cake); or one-hit wonders like Dalgona Coffee and Banana Bread. Around 38% of consumers are actively seeking new variety, within their preferred cuisines or with new international cuisines. And 39% are open to new brands and restaurants.

Going forward, the template seems to favour multi-brand formats that can rapidly evolve to cater to changing consumer preferences. Multi-brand companies by diversifying their portfolios, whether organically or inorganically, are securing steady revenue streams, mitigating risks, and enhancing consumer engagement.

In this context, the report cites cloud kitchens as a major game changer, as they can operate multiple brands within a shared infrastructure, thereby leverging higher operational efficiency, optimizing resource utilization, and accelerating time-to-market for new concepts.

India may not be Nikhil Kamath’s image of Singapore yet, where home kitchens are nearly obsolete, but make no mistake—this is one of the most exciting food service markets in the world. With a rapidly growing middle class, rising disposable incomes, and an evolving dining culture, Indian food service industry is on an unstoppable growth trajectory.

Whether it’s the rise of cloud kitchens, the explosion of international cuisines, or the shift towards sustainable dining, the Indian food landscape is undergoing a transformation unlike any other. As global brands, local giants, and innovative startups compete for a slice of this multi-billion-dollar opportunity, one thing is clear—India’s food revolution has only just begun.

For businesses willing to adapt, experiment, and cater to the changing palate of Indian consumers, the next decade promises a feast of opportunities.

Read More:

© Trade Promotion Council of India. All Rights Reserved.